Underwriting an Auto Garage Conversion | Office Hours

Everyone thought this deal had potential.

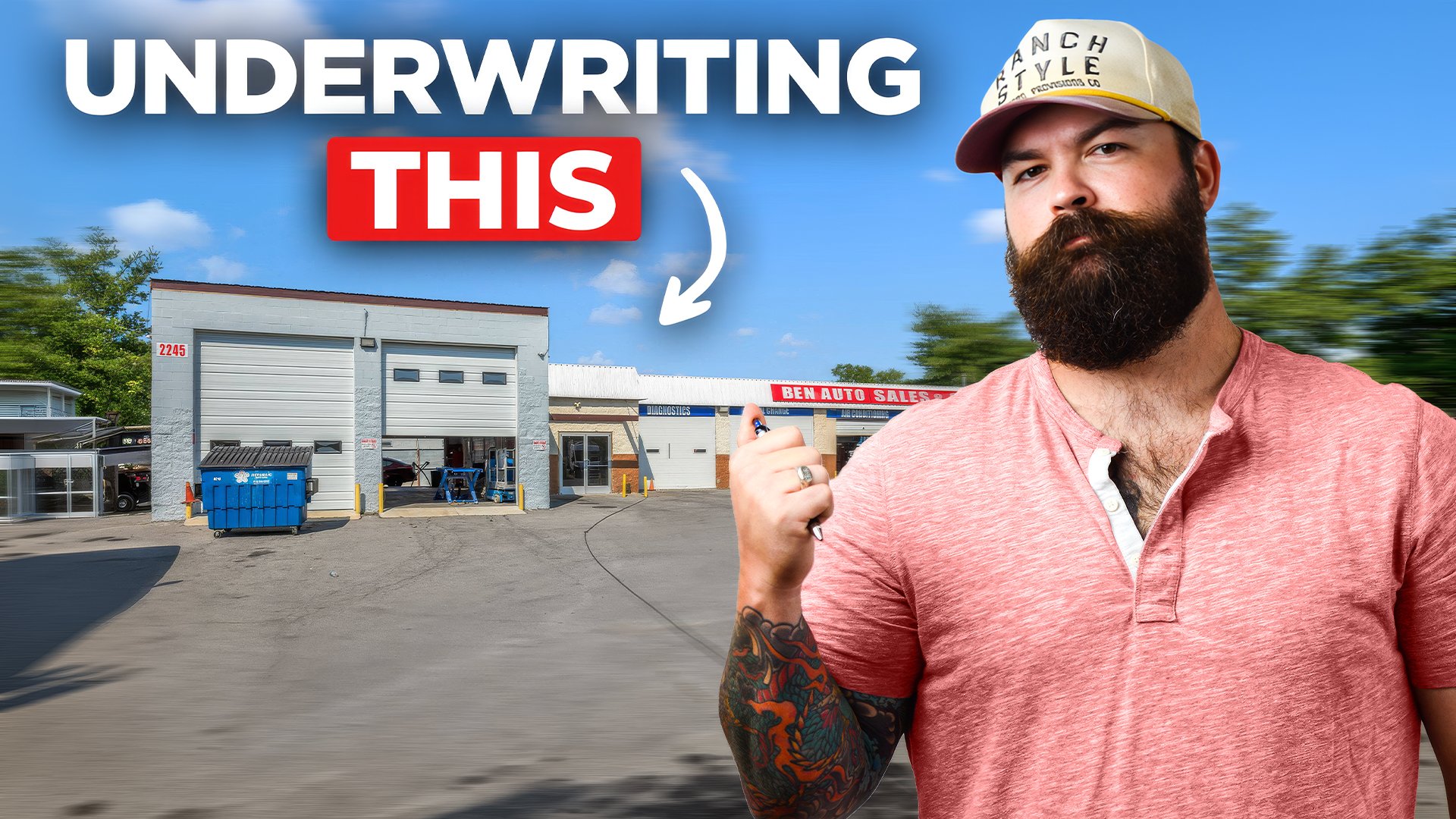

An auto garage in a high-traffic corridor, multiple bays, value-add upside—it checks all the boxes on paper. But when you actually sit down and underwrite it, the numbers tell a completely different story.

In this Office Hours, we walk through the full breakdown: how the deal was sourced, how to model rents and renovation costs, what the financing looks like, and where the deal starts to break. You’ll see exactly how small assumptions can turn into massive losses—and what the deal would need to look like to actually make sense.

If you’ve ever second-guessed a deal or wondered how experienced investors quickly decide to move forward or walk away, this will show you exactly how that process works.

Get commercial real estate coaching, courses, and community to jumpstart your investment journey over at CRE Central: www.crecentral.com

Key Takeaways:

Main Deal Conclusion

The auto garage near downtown Nashville is overpriced at $2.6M (~$480/sf).

Even after lowering price and rehab assumptions, the numbers don’t work at realistic market rents.

Tyler’s verdict: pass on the deal unless the price comes way down or there’s major zoning upside.

Why the Numbers Fail

Concept: convert 6 bays (~900 sf each) into micro retail.

Realistic rent assumption: ~$30/sf NNN.

At those rents, NOI is far below debt service, creating large negative cash flow and DSCR below lender minimums.

Only at extremely high, unrealistic rents ($50–$80/sf NNN) does it begin to pencil, which the market likely won’t support.

Value & Pricing Insight

For this kind of building and location, Tyler thinks $200–$250/sf (~$1.0–1.35M) is more reasonable than $480/sf.

LP/GP Structure Tips

Charge reasonable fees (e.g., 1% acquisition, ~2% asset management) to cover costs.

Simple structure he likes:

7–8% preferred return to LPs

Then a 70/30 or 80/20 LP/GP split, no complex waterfalls.

Salt Ranch Hotel Update

Tyler’s Salt Ranch Hotel in Nashville has soft-opened (April 1).

They’re adding a limited swim-club membership as an unmodeled but attractive new revenue stream.

Liquor license process was slow; they opened with beer first, full liquor coming online now.

About Your Host:

Tyler Cauble, Founder & President of The Cauble Group, is a commercial real estate broker and investor based in East Nashville. He’s the best selling author of Open for Business: The Insider’s Guide to Leasing Commercial Real Estate and has focused his career on serving commercial real estate investors.

Episode Transcript:

Tyler Cauble 0:00

This episode of the commercial real estate investor podcast is brought to you by my cre accelerator mastermind, where you'll get access to my step by step investment blueprint, essentially a library of resources on how to invest in commercial real estate. You'll get connected to a supportive community of other commercial real estate investors that are doing projects just like you. You'll get personalized coaching and feedback from me every step of the way. Go to www.crecentral.com to learn more. It's been a little while since we have gone in and underwritten or analyzed one of y'all's deals, and so today, that is exactly what we are going to be doing on this episode of office hours, Marissa Shapiro has submitted a deal, actually, I believe, here in the Nashville area, and we are going to take a look at it. I'm going to show you guys how I would approach it, how I would underwrite it, and we're going to use a piece of software that we actually developed for the members of the series, accelerator mastermind, which has completely replaced spreadsheets for us, which is kind of nice, because, you know, unless you are really living and breathing within spreadsheets, they can get a little overwhelming and complicated, especially depending on whose spreadsheet you're using, right? Everybody has a different version of spreadsheets that they like to use to analyze these deals. So that's why we created this piece of software. So you're gonna see today. We'll dive into it. We'll talk about everything that I would look at in this deal. And it's interesting because it gives you a lot more outputs on the back end, like including commentary about what will and won't make this deal work, which spreadsheets can't do. Oak and iron is saying, let's go. I never catch these lives. Welcome oak and iron. Glad to have you here every Tuesday, 8:30am central standard time we're going live. We're talking commercial real estate. So today we're going to be underwriting that deal. Let me go ahead and pull it up, share my screen with you guys, and then we will dive on in to what we are working on. Let me see here. All right, there we go. So Marissa saying she's stuck at the operating expenses pro forma piece. Let's see followed along the material looks like she was using the old spreadsheet, which we do still have available. You can get that in the deal analysis toolkit. So two deals for us to look at and underwrite. Let's pull up these URLs real quick. So this is very often the exact same way that you all are going to be finding deals and analyzing them, right? You're going to find them on crexy, on loop net, hopefully the pages load, and then you'll have to figure out, okay, how do we make this deal make sense? So it's a looks like an old auto garage. They're asking $2.6 million for it, 271 days on market. That's not exactly concerning when it comes to the commercial world, but it does tell me probably something going on here with it being 5400 square feet. Let's run the math on that. 2.6 million divided by 5400 square feet, give or take. I mean, it's 480 bucks a foot. That's an unbelievable price, way too expensive, way too expensive, and this is in Murfreesboro. That is crazy. That's a crazy price. Okay, all right, commercial property for sale with direct ingress and egress to Murfreesboro pike. Maybe it's not down in Murfreesboro. Maybe it's on Murfreesboro pike. Okay, never mind. This is closer to Nashville. When I saw that price, and I was thinking Murfreesboro, which is like a suburb, 45 minutes outside of town. It's like, That is insane, but this is actually right close to downtown, downtown Nashville. That is, all right, 5400 square feet under roof, perfect for another automotive venture or the retail business located in high traffic, high visibility corridor, 2.6 million will consider 12 grand a month. Troublemat. All right, let's look at some of the pictures here. Looks like it's in decent condition. I mean, block walls looks like you've got plywood on the roof, metal roof on this portion. Nothing special. This isn't an expensive build out by any means. I mean, this type of product, you could probably build it for like 150 bucks a foot, probably less, right? So always good to keep that in mind whenever you're looking at these deals, because if it makes more sense for you to just go buy land and build because it's substantially cheaper, like, look at that. I mean, I wouldn't pay 480 bucks a foot for that, and it's and it's coming vacant. So, I mean, you know, it's not like you've got a. Massive lease in place that would help.

Tyler Cauble 5:06

Let's look at the flyer. I'm gonna have to log in. I don't want to do any of that right now. Okay, let's take a look at the calculator and start throwing some of these numbers in. All right, so here's our calculator. For whatever reason,

Tyler Cauble 5:30

my computer doesn't like to switch the screen sometimes, whenever I switch over, okay, property, details, let's just call it says, deal. What do we say? It was about 5400 square feet. Give or take, 5417 I'm

Tyler Cauble 5:51

going to assume we're going to acquire it June 1. That's obviously fast, but we don't need to be exact, right now they're asking 2.6 million for it. Let me see if she says what she wants to do with it. Do

Tyler Cauble 6:24

doesn't say exactly what she wants to do with it. I wonder. Okay, Marissa is not here with us today. She's not saying what she wants to do with it, but I'm gonna make some assumptions here on let's see I'm mean, without knowing exactly what direction she's wanting to take, we have let's see 123456, bays Here, we could just assume we're doing, like a micro retail type of deal. Let's see how far. Yeah, it's like nashboro Village area. Ish, not a great area. Okay, so I mean, if we're gonna assume, hey, let's, let's turn these micro units, or turn these bays into micro units, you're gonna spend every bit of, I'd say, probably 100 bucks a foot, probably more, to be honest with you, because it's so small and like, your bathrooms are going to cost, what a bathroom is going to cost, whether it's serving 10,000 feet or 500 square feet, right? So let's, let's assume million dollars in capitalized rehab. That's closer to 200 bucks a foot. I feel a little more comfortable with that seeing the condition that the space is currently in. I mean, we're basically gonna have to completely redo it. Okay? Closing costs, I'm gonna assume about 1% in closing costs are down payment. We'll put down 25% for that notice how it just auto calculates everything for you. So nice. All right. Financing, we're gonna go with 75% I'm going to assume a 675, interest rate. You might be able to get a better interest rate today, I like to underwrite conservatively. I have seen some people starting to get into the high fives. Surprisingly enough, that doesn't ever happen in Nashville, though. I don't know why. All right, long term loan origination fee, 1% that's basically what the lender is going to charge you for doing the loan. Our minimum debt service coverage ratio target is 1.25 operating capital reserves. Let's do one month so we have that. I am in a model and interest only period for 1.5 years, because we've got a lot of work to do here. We're gonna have to get in here. We're gonna have to completely rehab it. We're gonna have to completely lease it up. I mean, we're gonna need some help from our lenders. For sure, we're gonna have six tenants. I'm not. I'm actually going to underwrite it as one tenant right now, just for the sake of making it simple, because I don't know exactly how these spaces are going to split up. So we'll just call this micro tenants. They're going to take up 5400, square feet, gross. I'm going to assume. I mean, here's the thing, if we take that 5400, square feet and we divide it into six bays, that gives us 900 square feet each. You know, at 30 bucks a foot, net, that's 2250 a month. I mean, that's affordable, right? So let's say that we're at $30 Square foot. The leases will start, let's say it takes us, like, a year to just get to a point where we actually are, like, comfortably leaf we're gonna go January 1 for fully leased 60 months, 3% rent bumps every year. We're going to do no ti allows, because we're just turnkeying this. Leasing commissions will assume 5% but depending on what type of deal you decide to do, I mean, you could throw a sign up in the front yard with a QR code that says, you know, hey, get on the wait list. You know, we had, we've had members of the accelerator mastermind do that and have their places fully leased before they even deliver the space, which is pretty cool. All right, baseline vacancy rate, we're going to keep it at 5% a bank is going to do that, so you want to have that in there anyway. We'll leave the second gen assumptions out for now. We will make this triple net so they are tenant responsible. 100% of OPEX will be reimbursable by tenants, and for OPEX on a property like this, especially once it gets this small and you've got, you know, some little things here and there. I'm gonna assume, like six bucks a foot for now, excuse me, all right, six bucks of fun.

Tyler Cauble 11:24

How that might that's probably too low. Let's go with eight. We're gonna increase that 3% per year too, all right, non operating expenses. I don't know if she's planning on doing this deal herself, or if she has let me look real quick. No, she's not here yet. Okay, so I'm going to assume no asset management fee for now, and I'll get to all his questions here in a minute as soon as we finish underwriting this deal. Asset Management if you have 0% capital reserves, you are going to want that we're spending a lot of money on the front end, so I'm assuming we're not going to have to have too much on the back end. So we'll do 15 cents a square foot. Now we are going to do a cost seg study that way we can do accelerated depreciation on this. We're taking it to office and retail. It's going to give us our typical ranges for what we can depreciate for each sector. So we're just going to enter through all of those exit assumptions. I would assume something like this. You'd exit maybe a seven half percent cap rate, maybe a seven probably lower, 1% in closing costs, 6% in commissions. And we're going to try and exit this by year five, no prepayment penalty. We'll just ignore the investor structures for now. I mean, we can get really complicated on this with a gplp, split preferred returns waterfalls, but we don't need any of that. So when I calculate this, the nice thing about the way that this works compared to a spreadsheet, it's actually going to give us a narrative on how all of this is going to work. You can print this off and actually use it as a pitch deck to your investors, if you wanted to. But let's see here. The biggest thing that I always go to look for at first is the risk considerations. So year one debt service coverage ratio is point two of point two. 1x is below typical lender minimums. Okay? We figured that because we're going to be under construction and then we're going through Lisa negative cash flow of $525,000 over five years, requires working capital reserves. Ooh, that means that our rent does not remotely cover what we needed to single tenant represents 100% of rent. That's fine. I mean, obviously we know that we're going to have six tenants, so we just underwrote it as one. Underwrote it as one single tenant dependency creates lease expiration risk. Yes, it does. Okay. Wow. Total cash required to close and carry $5.9 million interest, carrier reserve. That can't be right, 4.92 point nine total down payment $900,000 does not reach a one to five times debt service coverage ratio,

Tyler Cauble 14:17

negative cash or negative cash flow is really high. Wonder why? Well, let's go to our annual cash flow and look at it. Well, I mean, there it is, right. There we're bringing in roughly, you know, at stabilization, 160,000 a year. Our total income is 200 grand. Our operating expenses are 44 grand. Noi becomes 155 but our total debt service is 246,000 a year. So we are losing a substantial amount of money on this deal, substantial, and that's because. Is what I think that we could rent it for, compared to what it's being asked. What is being asked is just not realistic. So let's get into this, and we'll start messing with some of these numbers. Again, I don't think this property is worth 2.6 million. Be very honest with you, I think it's probably worth closer to maybe 1.8 million. And I think that's being generous as well. I maybe on the capitalized rehab side of things, we say, hey, look, we just can't make this super fancy. We've got to get it cheaper. We come in at closer to maybe 750 instead of a million. All right, let's see what that looks like. I

Tyler Cauble 15:54

so our purchase price is one eight. Our loan amount is 1.9 total equity required is 696, baseline vacancy, triple net mode, depreciation, operating reserve, or operating reserve, just keeps coming in too high. I'm trying to figure out why it looks like that. Because it shouldn't be our operating reserves shouldn't be that high, unless I put something in wrong. I

Tyler Cauble 16:27

do a fixed amount, 14 grand.

Tyler Cauble 16:36

No, that's not changing it. So this deal, I mean, we would have to triple the rents, essentially. I mean, because we're just losing so, like, our communal cash flows negative $200,000 and so the deal just never ends up penciling. So, you know, it's, let's look at the exit analysis. Oh yeah, it never works at any cap rate. Even in a five and a half percent cap rate, you're still losing money, tax deferred exchange. I mean, if we came in here and I made, I mean, let's just do this for fun, just to see what it ends up looking like, annual rent, $80 a foot. I mean, that's crazy,

Tyler Cauble 17:32

yeah, then it starts to work. Now we're, I mean, it's not good. You're still losing money. Even at $80 a foot, you're still losing money, but you actually turn cash flow positive in year two. So there's, there's a fine line to be made. And if I was going through this deal and doing this myself, that's what I would start playing with. It's like, okay, what rent rates make this work? And Is that realistic with the market? That's also incredibly important, just because it works in a small because it works in a spreadsheet doesn't mean it's going to work in real life. So just because I'm in here manipulating these numbers and, you know, getting to 50 bucks a foot and seeing if that works doesn't mean I can actually realistically go out and get 50 bucks a foot, but we do like to underwrite it until we see, like, Okay, what would the numbers have to be in order for this deal to work? And at 50 bucks a foot, it turns cash flow positive in year 280, $4,000 right? That's great. We still have such a negative in the first year that it still doesn't technically start throwing off cash until year three, as we can see right here. So I mean, the thing is like, do we think 50 bucks a foot triple net is going to be realistic for tenants now, with $8 a foot in triple net expenses, that's 58 bucks a foot times 900 square feet, that's $4,350 a month in rent. And I just don't think that that's remotely achievable for the tenants. So really, what it comes down to this property is overpriced. I think that at 5400 square feet, it's probably worth maybe 200 bucks a foot. So we're talking closer to 1,000,080 maybe you could start pushing 250 bucks a foot. It depends on what the underlying zoning is. And obviously we're not analyzing that today. We're just looking at we're just looking at this building and what's existing if it has some sort of crazy zoning underneath it, well then, yeah, I mean, it could be worth a lot more, but that's not what we're looking at today, right? So it's so important to go through the numbers, because you look at a deal like that and you're like, oh, this could be really cool. We could get it into micro units. We could make it work the you know, there's there's this angle on this angle and this angle. But as we just saw, like the the narrative on the deal, it doesn't work unless you're able to get an unrealistic market rate. So I would throw that deal right out the window. All right, let's get. Else questions. Ted is saying, Good morning. Thanks for being here, Ted, thank you for being here. Man, appreciate you. Appreciate you joining us. Nick is saying, Tyler, we asked a question on this live a few months ago about leasing our first property. We sent three leases over the past few months ourselves, and the building is now full. Thank you for the tips. Congrats. Nick, that's awesome. Man, that's really great to hear. He's saying, our on our next deal, if we're not charging GP fees, what's a fair LP, GP split 7030, or should we charge fees to balance it out while keeping it attractive and simple for investors, that great question, man, you know what I like to do honestly, charge the fees, because anybody's going to charge the fees anyway, and honestly, those are to keep the lights on. They're to cover a lot of your costs. Like, we charge a 1% acquisition fee, right? I mean, that's not nobody's getting rich. If we buy a $10 million property, it's 100 grand, like, nobody's getting rich off of that. That's going to cover a lot of our expenses of going into that property, right, all of the pre diligence and stuff like that. And, you know, my team and my time working on that, and same for you, the asset management fee. Nobody's getting rich on that either. It's typically 2% of gross revenues. I mean, if you're bringing in, you know, a million dollars a year. You're still talking about $20,000 a year. So it's, it's not that much and so, but it helps cover your expenses as an operator, which is incredibly important, right? You want to make sure that you're not having to come out of pocket to keep everything floating while you're waiting on the deal to turn a profit. So what I would say is, it all depends on the actual returns of the deal. Right? It could be 8020 it could be 7030 but it's gonna be somewhere in that range. I offer our LP investors a seven to 8% today. We used to offer a 6% preferred return, but seven to 8% preferred return today, and then it's just a pair of pursue split, right? So then it's 7030 thereafter. So they make a 7% return, 8% return on their money, and then we split it 7030 or 8020 thereafter. Super simple. Like, very easy. Like, we don't get into the waterfalls we don't get into really over complicating things. I think

Tyler Cauble 22:20

that you can just start to lose investors that way. And I just don't think that it's worth it, you know? I mean, also, I don't want to sit down and run calculators and do math all the time to figure out how much more money I should be making compared to my investors. Like, I just like it very simple. And my investors love that, right? They know, like, nothing's confusing them. They know that they're probably not getting screwed at any point. It's a, it's a, anybody can run that math. If we have $100 the LP gets 70, and I get 30. Very easy, right? And, you know, we like it that way. Husney, hard neck gaming is saying present, welcome. Thanks for joining us live, guys. Let me know in the comments, if you are enjoying going through the underwriting process, the deal analyzing process with me more. You know, we haven't done that since we did the 30 deals in 30 days back in the fall. So that was our first real deal to analyze. If that is something that you guys would like to do more of, let me know in the comments. Happy to do it. We could start adding something in like that. You know, every couple of weeks, you guys could submit deals, and I'd be happy to run through them with you. If not, I'll just keep bringing presentations and teaching you guys live and having fun that way. I've got to get back to the hotel. It's been a great couple of weeks to catch some of you all up. We did our soft opening for salt ranch on April 1. Really excited about that. You know, we've been working on this hotel for years, so it feels great to finally open the doors for other people to come and enjoy. It's been a lot of fun, because you're basically starting a business, right? This is very different from your typical commercial real estate, like, yes, we own the property, but we're also running a business and a brand. It's called the salt ranch Hotel. If you're ever in Nashville, feel free to check it out. We'd love to host you, but we're working right now on the swim club. We're going to have a Soho House style, you know, membership to the hotel, which is going to be really neat. We've got a massive wait list for that already because we're only opening up 100 memberships for that because we want to be very protective of the guest experience. But that's an additional revenue stream that that we will have that, you know, we actually didn't even underwrite, because it wasn't something that we had considered. We just figured, oh, it's just going to be for the guests. And then people started asking about, hey, who's going to have access to the pool? And we figured, you know what, let's do the membership. So that's that's been a lot of fun working on that. We finally got our liquor license last week. I mean, if you have never gone through that process, it is an unbelievable pain. You like? This is probably just in Tennessee. Every state's different. But in Tennessee, you cannot get your liquor license until you have passed your full health code inspections. Well, you can't pass health inspections until you're fully complete and finished. So like the place has to be ready to open, and then you have to pass your health inspections, and then you can pass your liquor inspection. So you basically get open without a liquor license. So we opened with beer. We will have our liquor orders coming in today. We have our first event at the hotel tonight for the Nashville area short term rental Association. I'm going to be speaking there about opening up a hotel and the difference between that and Airbnbs, which is pretty exciting. And then, you know, hosting everybody and having fun. So we've already had our first bookings. Of course, it's been a fun venture. So looking forward to hosting everybody that comes in town for Nashville events, for CRA accelerator events, whenever we have those in person here, because the place that we actually host is right down the street, so everybody will be staying at the hotel. Get to tell you guys a story about it. It's been a lot of fun. Awesome guys. Well, I appreciate you all for joining us in this week's office hours every Tuesday, 8:30am Central Standard Time. I'm going live come with your questions. I'll come with something to teach. We'll have a good time talking about commercial real estate. Appreciate you guys, and we'll see in the next one. This episode of the commercial real estate investor podcast is brought to you by my cre accelerator mastermind, where you'll get access to my step by step investment blueprint, essentially a library of resources on how to invest in commercial real estate you'll get connected to a supportive community of other commercial real estate investors that are doing projects just like you. You'll get personalized coaching and feedback from me every step of the way go to www.crecentral.com to learn more.