The Tax Code Was Written for Real Estate Investors

Most investors focus on making more money. Sophisticated real estate investors focus on keeping more of it.

In this episode, we break down the tax strategies commercial real estate investors use to build long-term wealth while legally minimizing taxes. From depreciation and cost segregation to 1031 exchanges and refinancing strategies, this conversation covers the exact framework many high-net-worth investors use to compound their portfolios faster.

You’ll learn:

Why the tax code favors real estate investors

How depreciation creates paper losses that offset income

The difference between straight-line and accelerated depreciation

How cost segregation can dramatically increase tax write-offs

Why investors use 1031 exchanges to defer capital gains taxes

How refinancing creates tax-free liquidity

The four pillars investors use to build and preserve wealth

Common tax strategy mistakes many investors make

How commercial real estate helps create generational wealth

Whether you’re buying your first deal or scaling a portfolio, this episode will change the way you think about taxes and investing in commercial real estate.

Get commercial real estate coaching, courses, and community to jumpstart your investment journey over at CRE Central: www.crecentral.com

Key Takeaways:

The tax code favors real estate investors by design

Post‑1986 tax rules intentionally incentivize buying, improving, and holding real estate because it creates jobs, economic activity, and a stronger tax base.

Wealthy investors often invest in deals primarily for tax benefits, not just for cash flow.

Most investors use a basic, suboptimal “W‑2 style” approach

Collect rent → deduct expenses → pay tax on what’s left (Schedule E).

Use straight‑line depreciation (27.5 years residential, 39 years commercial).

Occasionally do a 1031 exchange, but still eventually pay large capital gains and recapture.

This leaves a lot of tax advantage on the table.

Four key tax pillars for real estate investors

Depreciation (Pillar 1)

Non‑cash “paper loss” that offsets real income.

Only the building and improvements depreciate, not land.

Example: $1M commercial building straight‑line over 39 years ≈ $25k+/year in deductions.

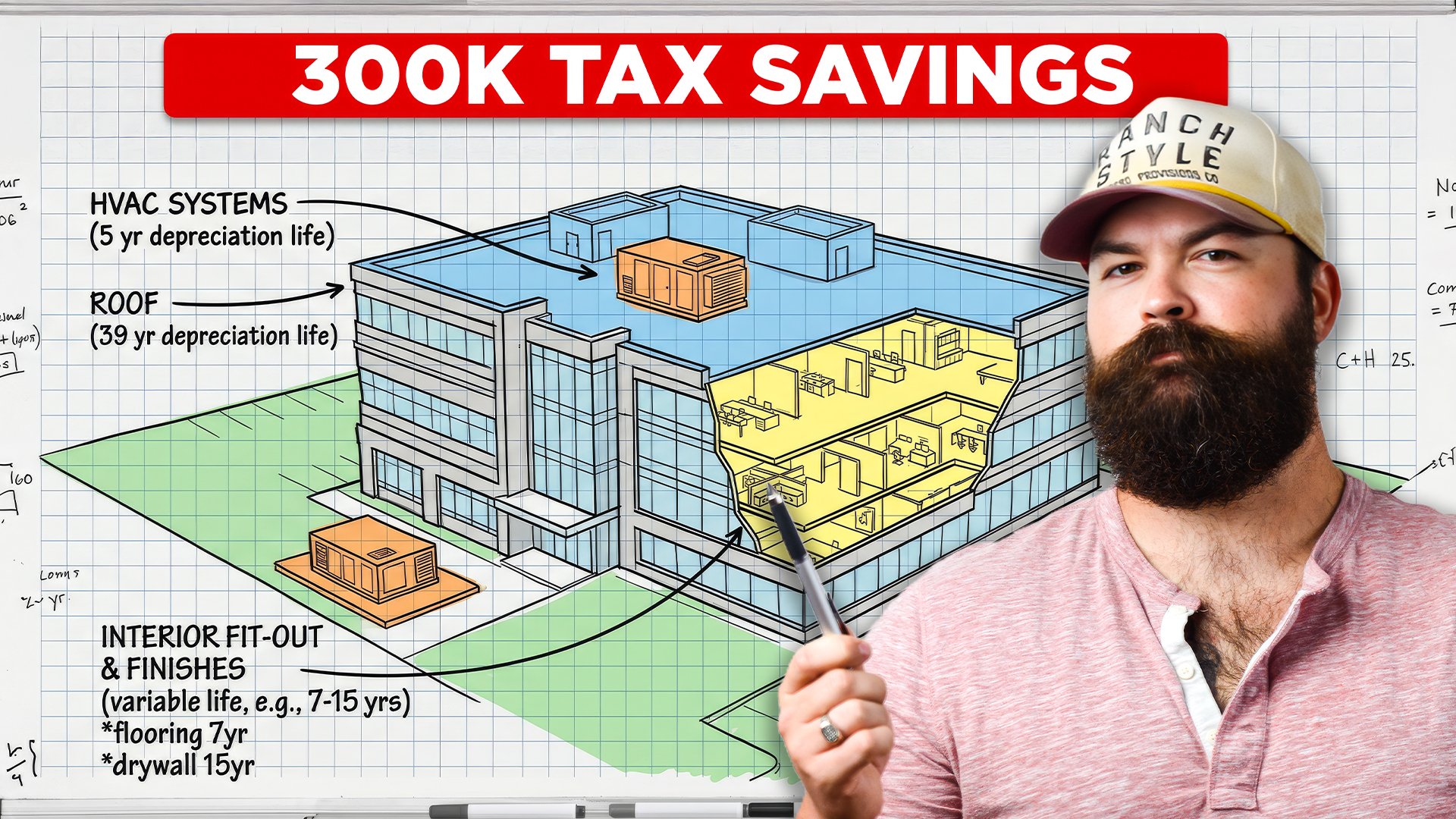

Cost Segregation (Pillar 2)

Engineering study separates components (HVAC, finishes, site work) into 5/7/15‑year schedules instead of 39‑year.

Enables accelerated and bonus depreciation—much larger deductions in early years.

Example: $1M building can create $200k–$300k+ in year‑one deductions vs. ~$25k with straight‑line.

Tyler’s example: $485k office → about $120k year‑one depreciation using cost seg.

1031 Exchanges (Pillar 3)

Sell a property, roll proceeds into like‑kind real estate, and defer capital gains + depreciation recapture.

Must:

Identify replacement within 45 days.

Close within 180 days.

Use a Qualified Intermediary.

Allows a multi‑deal compounding engine: keep equity working, reset depreciation on each new asset.

Example: Land bought at $618k, sold for $1.575M (~$900k gain). 1031 avoided $200k+ in taxes and rolled all equity into a new, cash‑flowing deal.

Borrowing Against Appreciation (Pillar 4)

Use cash‑out refis to pull equity tax‑free (loan proceeds ≠ taxable income).

Keep the asset, keep the income, access liquidity, and avoid triggering capital gains.

Over time, combined with 1031s, this supports long‑term wealth building and legacy planning.

Generational wealth & step‑up in basis

If an investor 1031s repeatedly and has large embedded gains, when they die, heirs get a stepped‑up basis.

Result: decades of capital gains can be effectively erased for heirs (no capital gains tax on prior appreciation at death).

Strategic takeaway: You need the right tax team

A real estate‑focused CPA/tax strategist is critical—many general CPAs:

Don’t suggest cost seg.

Misunderstand when/why to use it.

Tax planning should be proactive and strategic, not just end‑of‑year compliance.

Practical investor playbook (how his partner paid ~$0 on $1M+ net income)

Stack all four pillars:

Ongoing depreciation.

Cost seg + bonus depreciation to load losses early.

Use 1031 exchanges to keep equity compounding and reset depreciation.

Refi to pull cash out tax‑free instead of selling.

Result: very high income, minimal federal income tax, fully within the tax code.

About Your Host:

Tyler Cauble, Founder & President of The Cauble Group, is a commercial real estate broker and investor based in East Nashville. He’s the best selling author of Open for Business: The Insider’s Guide to Leasing Commercial Real Estate and has focused his career on serving commercial real estate investors.

Episode Transcript:

Speaker 1 0:00

Speaker 1 0:00

This

Tyler Cauble 0:05

episode of the commercial real estate investor podcast is brought to you by my cre accelerator mastermind, where you'll get access to my step by step investment blueprint, essentially a library of resources on how to invest in commercial real estate. You'll get connected to a supportive community of other commercial real estate investors that are doing projects just like you. You'll get personalized coaching and feedback from me every step of the way go to www.crecentral.com to learn more. One of my partners netted over a million dollars this past year and paid effectively $0 on his taxes. Now, while I have never quite gotten to that point, I've saved a lot of money on my active income over the years by simply investing in commercial real estate, and so today I'm going to walk you through how he did it, how he was able to net that much in income and pay zero in taxes. Now, to start us off, I am not a CPA. I'm not your CPA. I don't pretend to be one on this podcast. So this is not tax advice. This is shared from my experience and what I've seen out there in the world. Go consult your tax professionals. All of this is legal. It is all permitted in the tax codes per the IRS. So if you are not taking advantage of the four pillars that I'm going to talk to you about today, you've got to start rethinking your entire tax strategy. We literally have investors in my development firm, people that invest in deals with me that strictly do it for the tax benefits. They don't want any cash flow because they're already making 234, $5 million plus a year. They're just trying to figure out how to protect the income that they are already making so they don't have to pay more in taxes. So we're going to be diving into today why the tax code was written for real estate investors, how it is written for real estate investors? All right, so this is pretty interesting. Again, $0 on over a million dollars in net income last year. It's not a tax dodge, it's not a loophole. He's not sheltering capital offshore. And here's the thing, it's it's not even particularly clever. It's not like this is something that you have to be, you know, some sort of savant or quant to be able to figure out this is literally in the tax code, doing what the IRS allows you to do. So let's dive into it and how to use it. Now, most real estate investors handle taxes in a pretty straightforward manner. All right? Me adjust my camera here real quick so that we can make sure you guys can actually see a lot of the stuff that I'm talking about. All right, there we go. So most real estate investors are going about it in what I like to refer to as the w2 approach, right? Which isn't wrong. It's just not the the most ideal way for you to go about taking advantage of everything that is available to you. Okay? So number one, you buy a building, you collect rent, and you pay taxes on the income. You treat it like a landlord, right? You file a Schedule E, you deduct your expenses. You pay what's left, right? Or you pay on what's left number two, then you depreciate the building on a straight line schedule, right? If you're buying residential or multifamily, you're able to depreciate a building on a 27 and a half year schedule. It is 39 years for commercial, which is absolutely absurd. So take your, you know, roughly what, $25,000 a year, so to speak, and move on. Okay, depending on the price of the building that you're buying, maybe at some point you'll do a 1031 exchange, right? You'll defer the gain on the sale. It's the most used tool. I love doing 1030 ones. We just helped one of our members of the accelerator mastermind do his first one, and it was pretty killer. He got into a 30,000 square foot mixed use building. So shout out to Chad. It's one of the most used tools in the tax game for commercial real estate. It's great, right? But it's definitely not the only one. There are way more options available to you that can be incredibly, incredibly helpful on saving your cash you pay the capital gains and depreciation recapture at sale. So watch a pretty substantial portion of the cash that you make to the government, right, send it back to them. Now, of course, you can continue doing 1030, ones until the end of time, kick the can down the road, as we like to call it, but at some point, if you do decide to sell, you will have to pay taxes on the gains. I have seen investors over the years. Maybe they did 234, 1031, exchanges. They built up a massive amount of capital off of a revenue. Relatively low investment in the first place, maybe one or $200,000 now they've got several million that they're walking away with. Well, they're going to be paying 20% on several million dollars. Think about that. You could be paying 500,000 $600,000 in taxes just for selling a property, because those capital gains start to stack so the investors that are paying almost nothing like my partner did last year operate on a completely different framework. So here's what that looks like. All right, the tax code treats real estate differently intentionally. It was written this way on purpose. This goes all the way back to the 1986 Tax Reform Act, which was which really codified structural advantages for real estate investors. So housing commercial development, property improvements, that all creates jobs, that stimulates economic activity, and it improves the tax base. So Congress wanted to incentivize real estate development because it generates a substantial amount of benefits for a community, right? So they're incentivizing you as the investor, as the developer, to go out and make this happen so that they can collect more taxes elsewhere. Think about it. I mean, if you build a 250 unit apartment complex. That's 250 people that are now able to move into the area. They're going to be spending money in the area, paying income tax. They're going to be working jobs in the area, which creates payroll tax, right? More income tax, right? There's all sorts of taxes that people create when they move into an area. So it's very lucrative for the government to incentivize real estate investors and developers to create more opportunities for people to live, work and play. All right, so here's the big distinction, your CPA handles the filing after the year is over, right? If you don't have a CPA that thoroughly understands how to actually work in real estate. And I'm always floored by this. I'm amazed at how many real estate investors reach out to me asking for referrals to CPAs, or how to find a CPA that actually understands real estate. Because they've never heard of a cost segregation study, their CPA has never brought it up to them, or their CPA says actually, you shouldn't do a cost seg study, and here's why. Now that's not to necessarily say that that's entirely incorrect, but here's the thing, if you have a CPA that is telling you you should never do a cost segregation study, you should be asking them why, and you should be getting a very detailed response for your tax portfolio, your tax situation, specifically, because if it's just a, oh, well, you have to play, pay, you know, recapture at sale. That's not a good excuse, right? That, to me, says that CPA probably doesn't understand what a cost segregation study is real a real estate tax strategist, on the other hand, a CPA that specifically focuses on real estate, which, by the way, is it's hiring a CPA that focuses on real estate is very similar to hiring an attorney or hiring a real estate broker. You're not going to hire a commercial real estate agent to sell your house. You're not going to hire an environmental attorney to represent you in a speeding ticket. Right? There's all sorts of different classifications within these and CPAs are no different. A CPA that's really, really, really good at handling everything for your business may not necessarily be the same CPA that should be handling your real estate portfolio. So there's four pillars that we're going to dive into. Each one is valuable alone, but when you start to stack them, like my partner did, that is how you get to a point where you could effectively pay nothing in taxes, despite, I mean really, at over a million dollars in income, he would have paid two, $300,000 in taxes, so quite a bit of capital saved there, all right. Pillar number one is depreciation. This is the paper loss engine, right? You're writing off losses on your property because you're depreciating it that are strictly on paper, right? You're not actively losing that cash. So the IRS allows you to basically depreciate your building. They're going to say, hey, over time, your building is going to become worth less and less because it wears out, right? Your roof is going to age every single year, and at some point you're gonna have to buy a new roof, right? So you get to claim that as a loss against real income. So let's do a million dollar building. For example. If you just straight line, depreciate that over 39 years, you get to write off 25 a little over $25,000 every single year, right? That's just straight line, right? So just. For having bought the building, you get to write off $25,000 every single year. Now there's a catch. Land does not depreciate. You can't depreciate land. Only physical improvements to the property can actually be depreciated. That means the building, that means any of the infrastructure serving the building, that's what can actually be depreciated. So if you buy a piece of land with a shack on it for $12 million and the land is worth 11 million you can still only depreciate roughly a million dollars. All right, so make sure that you understand that before you go into it. So essentially, this pillar is, I bought a building. It went up in value. The tax code lets me claim it as lost value every single year. That's pillar number one. So depreciation offsets real income with a paper loss. Again, just for having bought it, you get to just depreciate it kind of nice, right? So building went up. Tax bill went down. Let me get over here to some of y'all's questions real quick and see what we've got going on. So Carl is saying, Hey buddy, getting ready to purchase a flex space building zone light industrial. Congrats, Carl, that's really exciting. Happy for you, man, Flex is one of my favorite asset classes. Such a good, good building, that's for sure. They're very, very utility. Ricker to say good morning from Santa Fe, New Mexico. Tyler, thanks for all you do Absolutely. Rickert, glad to have you here walk us what's going on, man, good morning. Good to see you. First American property or partners. First American partners. Good morning. Happy Tuesday and Ted is saying good morning as well. Happy to have you here. Guys, thanks for joining us. All right, let's get back to this. So pillar number two is cost segregation. I mentioned this earlier. If you are not familiar with this term, this is the magic pill when it comes to commercial real estate, this stuff is amazing. I love Cost Segregation studies. They can be a total game changer in your life. All right, so really, what a cost seg study does you have an engineering firm come in and they break the building down in all of the individual components so that you can depreciate those on a faster schedule than you could a straight line depreciation over 39 years. Because if you think

Speaker 1 12:29

about it,

Tyler Cauble 12:30

straight line appreciation 39 years. Okay, is my HVAC unit going to last 39 years? Absolutely not. So, why are we depreciating it over 39 years? Because you're going to probably buy three, four sets of HVAC units in that time. All right. So this, breaking it down into these components allows you to depreciate over some stuff, over five years, some over seven, some over 15, instead of that 39 years, so without a cost seg, going back to this straight line depreciation on that $1 million building, our year one deduction would be roughly $25,000 when you do a cost sec, when you take advantage of some of this bonus depreciation that same $1 million building, you could get up to 200 to $300,000 in a year one deduction. It's pretty wild. I bought a $485,000 building, small building, very approachable for many of you, right? It's where my office is, very small. I like it pretty nice. Year one, we wrote off $120,000 of depreciation by doing a cost egg study. Pretty remarkable. What you are able to do with some of this. Okay, so like I said earlier, if your CPA has never mentioned a cost seg on a property you've bought, they are probably not the right strategist for you to have on board. Like I said, real estate CPAs are built different so most investors will take that 25k a year. Whenever I see that happening in somebody's portfolio, it's just such a travesty to me. There is a reason that most real estate, like professional real estate investors, end up holding their deals for five to seven years, because the majority of the tax benefits that you get occur in that first five to seven year period. Most commercial loans line up with that five year period. So that allows you to maximize to the fullest extent, not only the value add play and but also the depreciation. Then you sell it. You 1031, exchange into the next one, and you move on. All right. So first American partners are saying, What's the difference between straight line and accelerated we are diving into all of that right now. DP is saying, Does the cost seg get recaptured? It does. It does. And we will talk about that a little bit more.

Speaker 1 14:59

So.

Tyler Cauble 15:00

So pillar number three is the 1031, exchange. This kind of gets into that recapture. All right, so when you sell a property, you roll the proceeds into a like kind property, and you're able to defer those capital gains. You're able to defer that recapture. All right, if you ever do sell, there is a portion, there's a recapture rate, I think it's around 25% of the total depreciation that you'll have to pay back. All right. So even if, I mean, of course, it depends on your specific situation, the property, your tax portfolio, whatever it looks like, even if you do decide to sell and not do a 1031, exchange, you're only paying 25% of that back. All right, give or take. Talk to your CPAs. So deal number one, let's say we sell it. We make a $500,000 gain. We roll that forward into deal number two, and then keep it going. We'll do deal number three, deal number four, number five, continue rolling it forward through 1031 exchanges. This is why this is such a powerful, powerful asset for real estate. Now, you can't sell stocks and do a 1031 into real estate. You can't sell gold and do a 1031 into real estate. You could sell gold and 1031 into silver, right? That's a like kind asset. You could sell a residential home in 1031 into an apartment complex, or 1031 into a flex building. Real estate is all a like kind asset class. Okay? So your tax bill on each sale will be $0 because you are deferring those gains. They roll forward. They keep working for you in the next deal. And I get to an example here in a minute of a deal that I did with a partner, I guess, a couple years ago now at this point. So we have plenty of videos on this channel that go further into 1031, exchanges, the deadlines, how to go about doing it the right way, all of that kind of stuff. But high level when you sell a property of 45 days from the day of sale to identify a replacement property. Now it could be two or three. Could be more than that, just depends on how you decide to actually go about the 1031 exchange. I highly recommend, if you are interested in this, to go watch the videos that we have done on 1031 exchanges. You then have 180 days from the sale to close on that replacement. And then, if you do everything by the book, you have a Qualified Intermediary that guides you along the way. You will pay $0 at the time of sale, pretty phenomenal. So instead of paying that money to the government, you actually get to keep it working for you. Think about that. I mean, you know, even if it's only 200,000 hours, if you're getting a 10% return on that, you're making $20,000 a year instead of paying it to the government and making nothing. Right? Twist my arm so pillar three turns a one time tax win into a multi decade compounding engine. You can keep this going forever. This is how people really build wealth in real estate, because, and you'll see this in my example here in a minute, you can get into the your first deal for 100 or $200,000 value. Add maybe you walk away with $500,000 in equity. Roll that into the next one, then you'll walk away with 750 or a million dollars in equity. Roll that into the next one, and now you're keeping that cash in play, making more and more and more every single time you 1031 and the beautiful thing about it, every time you do a 1031 exchange, we get to go back and restart our depreciation and Cost Segregation clock, right? That's why investors will sell a deal every five to seven years, roll that money forward into the next one and restart the depreciation clock, because all of a sudden, just because they bought a new building, they get all the tax benefits over again. Okay? Pillar number four. This is where it gets really unfair, in a good way for you as a real estate investor. And this is actually how the wealthiest individuals operate their entire portfolios, not just in real estate, but also stocks, also against their companies, whatever it is you can borrow against your appreciation. You guys are probably familiar with the burr strategy. That is exactly what this is, right? You can do that on a very large scale if you wanted to. All right, that creates tax free liquidity when you go and you refinance a property and you do a cash out refi, those loan proceeds are not income. It is a loan. It is not taxed. You don't have to pay any tax on it. So if you sell the asset, capital, Gains Tax gets triggered, depreciation recapture is due. State taxes may apply. The asset is gone, right? You no longer have that income coming in. However, if you do a cash out refi zero tax, because it's not income, the asset stays in the portfolio, you get to continue riding the appreciation wave. Now, again, there's something to be said here, too, for not being able to restart your depreciation clock, but it all depends on your portfolio strategy. We work with family offices and high net worth individuals on what assets we should sell, what we should keep all the time. It's a lot of fun. It's actually like a puzzle to me. So it's one of the things that I enjoy the most about getting to work with individuals at that level. The equity keeps compounding, and then you just get to do it again and again and again. And here's what's interesting. I mean, if you're building real estate for a legacy, maybe you have kids, you have family that you want to leave this all behind for. At death, the heirs inherit a stepped up basis. So let's say you 1031, 10 times, and you owe $10 million dollars, or you you have your gains are $10 million and so your tax would be probably, what, 2 million right decades of embedded gain permanently erase because of that step up basis, so your heirs don't have to pay that. They actually get a step up basis, meaning if they decided to sell at your death, they don't have to pay the capital gains tax. They'll still have to pay plenty of taxes, but they don't have to pay the capital gains tax, because there's technically no capital gains for them anymore. So that's how generational wealth gets built. That's how it actually works. You kick the can down the road. You leave the assets to your kids, to your family, friends, whomever you're leaving them to, they get a step up in basis, and they never have to worry about paying those capital gains tax. So let's get back to my partner. He didn't use a single pillar. He stacked all four of these, which is completely within your abilities, within your rights to do as a real estate investor. So he took, he took advantage of depreciation, right? That offsets some rental income year over year. Right, the baseline for all of your tax benefits was kind of running quietly in the background, all right. He did cost segregation, right, front loaded everything into year one. Right, over $200,000 in paper losses applied against real income. And here's the thing, depending on the type of asset you buy, you can actually get more depreciation, right, because equipment depreciates largely in that first five years and also qualifies for bonus depreciation. So that's why you'll see investors buying car washes at a five and a half percent cap rate. You're like, Well, hell, that doesn't make any sense. Why would anybody buy a car wash at a five and a half percent cap rate? Well, it's a ton of equipment, so they get to depreciate a ton in that first year. So if you're trying to save a million dollars in tax liabilities, and you're able to write that off in year one, the five and a half percent cap rate, which essentially is a five and a half percent cash on cash return, give or take, if you pay all cash, that's just gravy on top of it, right? Because when you start to add back in the amount of cash you're actually saving by just having bought the asset, you could be looking at 20 to 30 to 40% plus returns effectively, just by doing that. All right, if

Speaker 1 23:28

you take

Tyler Cauble 23:29

advantage of a 1031 exchange, you can keep pushing the gain forward. All right, so, I mean, imagine you buy a property, you have a lot of gains. You sell it, you do a 1031, exchange. You pay nothing in taxes, you start your depreciation, you do a cost segregation study. And then after a year or two, three years, you've done value add. You do a cash out refi, right? You pull out cash tax free, you go buy another property. That is how you start snowballing all of this wealth building that is possible for you in commercial real estate, all right, so like I said, over a million dollars, absolutely not in net income zero in federal income tax. That's how the four pillars can work together. So here's, here's pillar three in action. This is what a partner of mine and I did a couple years ago. So we bought some land for $618,000 our down payment was around 200 we probably put another 40 or 50 into it just to rezone it. And because of that rezoning, we were able to sell it for 1,000,005 75 right? We held it for 18 months, and our gross gain was a little over 900 grand. Right now we're both in that 37% tax bracket, so we would have owed over $200,000 in taxes if we hadn't done a 1031 exchange. However, we did a 1031 exchange, kept all of that cash working for us and didn't have to pay $1 to the government.

Speaker 1 25:00

It

Tyler Cauble 25:00

now, that initial $200,000 investment, since we increased our equity, since we sold, didn't pay any taxes, rolled it forward into the next deal, will net us between 20 and $30,000 a month. Think about that. That $200,000 is netting between 20 to $30,000 a month because we decided to grow the equity, sell 1031 exchange, and now we're in something that's more stable. Think about that you could never, ever. I mean, if you found something that you could buy for 200 grand, that's going to net you 20 or $30,000 a month, basically 10% per month. I want to invest with you. It's very rare to find deals like that, but that is the power of leveraging the abilities that you have in real estate, right? So we made one decision at closing, let's just do a 1031 that's not a tax strategy. That's just literally reading the instructions, right? We didn't think creatively. We didn't do anything outside of the box. We just did what we are able to do in commercial real estate. All right? Most investors stop at pillar one. They just do the depreciation. That's crazy to me, especially if you're buying a building, you're holding it for five years, and you're straight line depreciating it over 39 you're only going to take advantage of five out of 39 years to write off, right? Most people do that. Few people do a cost segregation study, which really starts to stack it, and it always surprises me. So if you don't know anything about cost segregation, we will be talking more about it next week. We also have some other videos on that on this channel. Highly recommend you go and check those out. Ask your CPA about doing a cost segregation study. There are some people that will say, Oh, well, the deal has to be of a certain size for you to justify a cost seg study. There are a few grand, like three to $5,000 to have it done. We justified it on a $485,000 office building. All right. Then there's the 1031, exchange. Some people do that as well, right? It's something that I always recommend. Now, there are times where you might want to look at what your tax liabilities are. If you have a ton of depreciation, of write offs, and you just need the cash, you might be able to actually offset the gains by doing that. Again, talk to your CPA. But then very few get to the point where they are borrowing against the appreciation, against the equity that they've built up in a property, and then just hold it for a while, right? Like I said, it requires a CPA that actually understands real estate strategy, not just real estate real estate strategy. You want a CPA that is proactively working with you that is helping you plan ahead, right? Those are two different jobs, so make sure you know what you are paying for. The tax code is literally set up to reward investors who operate in this way. They want to incentivize you to buy more real estate, to improve more real estate, to keep the market rolling. All right? So it was literally written for investors. The tax code was the ones who know it and the ones that do it right pay very little in taxes compared to those that don't. You don't want to be approaching your real estate tax situation, as if you're a w2 employee, you want to approach it as if you're an entrepreneur, as if you're a business, as if this is a professional undertaking. All right, so take those four pillars that I just taught you about and go out there and utilize every single one of them to the fullest extent. If you ever have any questions on that, that's why I go live every tuesday here for office hours, 8:30am central standard time to answer your questions about that. Now I help investors do this all the time through the CRE accelerator. Also consult high net worth individuals and family offices. If you're interested in joining the mastermind and working with me on your tax strategy and working on building your commercial real estate portfolio. Check that out at Siri central.com, the Siri accelerator. It's a lot of fun. All right, let's get to those questions your turn. I want to know because we've got some people jumping in the comments here. Has your CPA ever mentioned a cost seg study to you? Drop it in the chat. Let me know what your thoughts are. All right, let's see. Husney is saying, Good morning, guys. Good morning. Husny, good to see you here. The village elder class is in session. Absolutely it is. We are here. We are having a good time, and we are diving into everything. So appreciate you guys having me here. Ken is still asking, what's the difference between straight line and accelerated So Ken, the difference between straight line depreciation and accelerated depreciation? Straight line you get to write it off over 39 years. Accelerated means you get to write it off over five, seven or 15 years. So you get to write it off a lot. Faster, substantially faster. Dylan is asking, what are the tax advantages of investing in opportunity zones? That's a good question. I mean, it's it's different today, simply because we don't have the full capabilities that we used to have under opportunity zones, but typically, like when they first came out with them. So, I mean, obviously, talk to a an oz specialist with regards to this, because we took advantage of it when it was there. It's not really there anymore, or at least as much. But the theory was, if you had capital gains and you rolled them into an opportunity zone, and you met all the criteria, which, you had to spend a certain amount of money on the building to improve it, to make it happen. For you to qualify, you were able to, after a 10 year period, sell that property and effectively pull out all of your cash without paying anything in capital gains tax. Pretty powerful. And they were even allowing people to sell stocks gold, it didn't have to be a like kind asset for you to be able to take advantage of that. Now, things have changed. We're in a very different situation now. I think they have to renew it every so many years. And you know, the actual effective, I don't know, benefits of it have changed a little bit, so I would look into it more today. But you were there are still benefits to opportunity zones. I just don't think they're as good as they used to be. That's why you don't hear people talking about them as much anymore. So I think it's pretty interesting. All right, Ben is saying good morning. Thank you for the great information. Absolutely. Ben happy to provide it great to be with you guys as always on this week's episode of office hours, Tuesdays, 8:30am Central Standard Time Jump in with your questions. I'm going to be teaching you guys something tactical about commercial real estate that you can actually go and implement today. Let me know in the comments which of these four pillars you find most appealing that you are going to be utilizing most on your next deal, and I'll see you guys in the next one.

Speaker 1 32:08

This

Tyler Cauble 32:12

episode of the commercial real estate investor podcast is brought to you by my cre accelerator mastermind, where you'll get access to my step by step investment blueprint, essentially a library of resources on how to invest in commercial real estate. You'll get connected to a supportive community of other commercial real estate investors that are doing projects just like you. You'll get personalized coaching and feedback from me every step of the way, go to www.crecentral.com to learn more you.